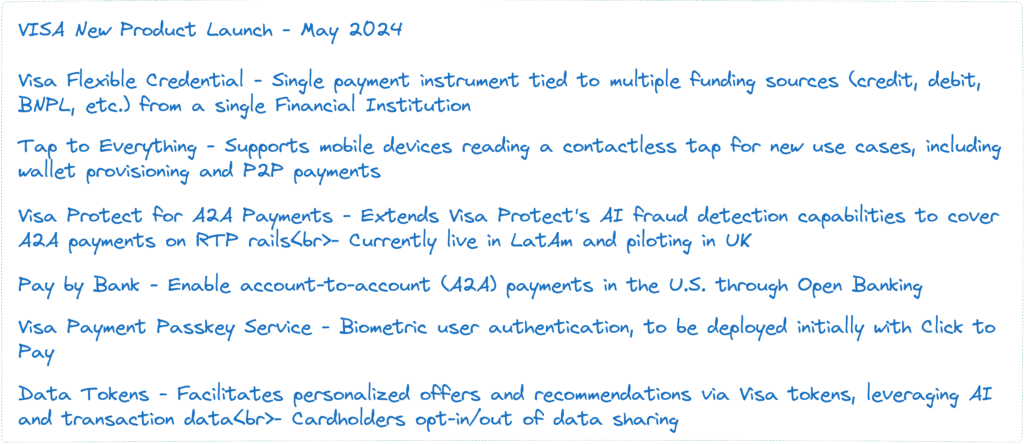

As digital payments continue to evolve at a rapid pace across the Asia-Pacific region, forward-thinking fintechs and banks in key markets have a unique opportunity to leverage Visa’s latest innovations around flexible credentials and data tokens to reimagine the consumer experience and embedded payment loyalty programs.

One Card to Rule Them All

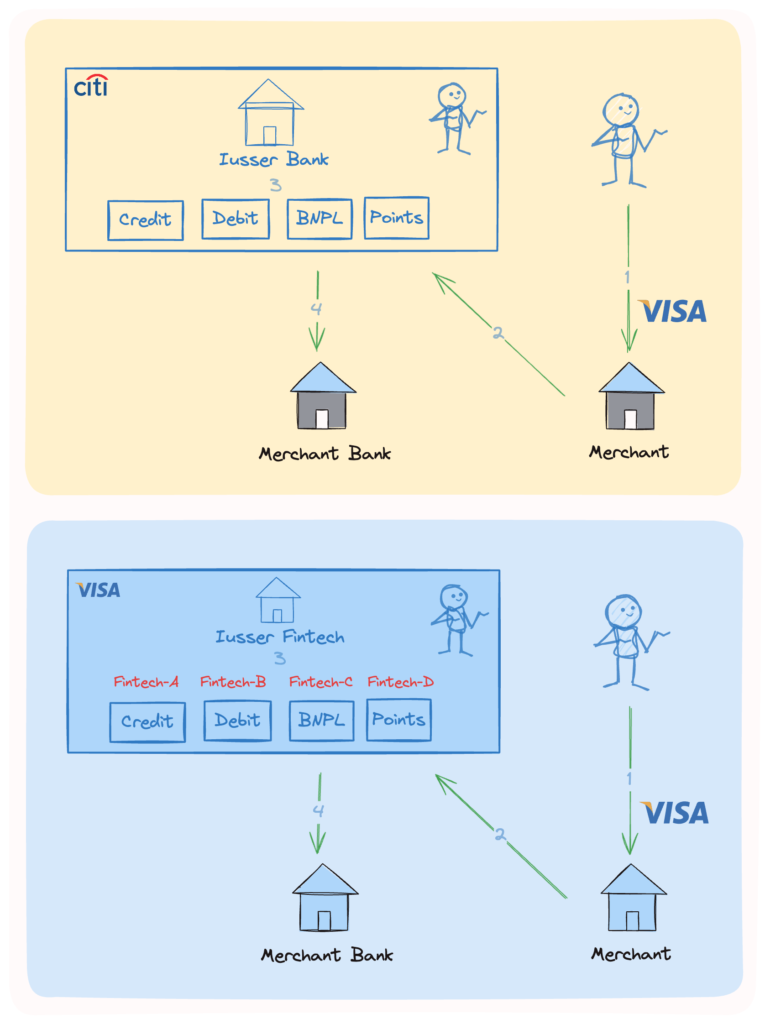

Visa’s Flexible Credentials is a game-changing technology that allows users to steer their 16-digit PAN to any available balance or spending limit, even after the transaction settles. Imagine paying for groceries with a single tap and then being able to move that expenditure to a different card with better rewards, switch to debit, or even split the payment across multiple cards—all without changing the original card used. This innovation, currently piloting in Asia and expected to reach the US by late 2024, significantly enhances the consumer experience by abstracting the complexity of multiple payment methods and rails.

Abstracting Complexity for Enhanced Loyalty

To consumers, using Flexible Credentials will feel like using a regular credit card, but behind the scenes, Visa’s infrastructure captures and routes transactions based on customer preferences. This reduction of the concept of a wallet down to just one card means that consumers can enjoy a seamless payment experience, while merchants and fintech players can focus on providing innovative solutions. For example, an innovative Fintech could partner with Visa and popular merchants to allow customers to opt-in to sharing their data in exchange for real-time, AI-driven product recommendations and discounts as they shop.

Data Tokens: The Key to Hyper-Personalized Loyalty

Visa’s data tokens let consumers control their data and receive better shopping experiences, powered by AI. By tokenizing payments, Visa removes sensitive cardholder account information from the payment flow, empowering consumers to have more control over their data. This innovative approach enables merchants to request consent from consumers to get more personalized offers, and consumers can easily review and revoke access to their data in their mobile banking app.

The most successful players will likely be those who can strike the right balance between delivering clear value to the consumer and merchant partners in terms of savings, convenience, and delightful experiences, while maintaining the highest standards of data privacy and security that Visa’s tokenization affords.

SO WHAT, for Issuing Banks and Fintechs?

For now, the steering power of Flexible Credentials is limited to the issuing bank level. This means that if your primary card is issued by Citi bank, for instance, your ability to steer that payment towards another payment source will be limited to other Citi-issued cards and products. However, it’s possible that Visa may offer a steering wheel that permits (or even incentivizes) you to steer away from your issuing bank to another bank in their network. This could potentially disrupt the old familiar banking model, allowing Visa to position itself as your wallet’s steering mechanism before tech giants like Apple and Google can step in. This could be extremely challenging for Visa as they would be bound by issuer banks and this is where partnering with fintechs and building a bouquet of products could help neo banks gain advantage with differentiated offerings. Here card schemes have unique strength, where they own the last-mile connectivity between end consumers and merchants.

The Battle of the Browser

As we move towards a world of real-time, AI-assisted financial co-pilots and agents, the browser experience will play a crucial role in shaping the future of financial services. Take Kudos, a start-up that automatically activates when it detects a spending interaction to steer the consumer to the payment method offering the best rewards for the transaction at hand. If you have heard / used Curve, you get the drill. Imagine if Apple and Google were to integrate similar technology into their browsers, allowing them to optimize rewards and even execute contracts on behalf of the consumer.

The Future of Fintech in APAC

As we look to the future, it’s clear that fintech players in APAC, will need to adapt to this new landscape. With the rise of digital wallets and innovative payment solutions, the battle for consumer control will only intensify. Will Visa’s Flexible Credentials and data tokens be the game-changer that sets the standard for fintech innovation in the region? Only time will tell.

Innovative Approaches for Fintech Players

So, what can fintech players do to stay ahead of the curve? (No pun intended)

Here are a few innovative approaches to consider:

- Develop Browser Plug-ins: Create browser extensions that optimize rewards and steer consumers towards the best payment methods, similar to Kudos.

- AI-Assisted Financial Co-Pilots: Integrate AI-assisted financial co-pilots and agents into platforms to provide personalized experiences for consumers.

- Leverage Visa’s Data Tokens: Use Visa’s data tokens to empower consumers and provide better shopping experiences.

- Collaborate with Merchants and Banks: Develop innovative loyalty programs and rewards schemes through strategic partnerships.

The future of fintech is exciting, and it’s up to us to shape it. Let’s work together to create a world where consumers are in control, and fintech innovation knows no bounds!

References;