Measuring the performance of investing in private markets has always intrigued me as little information is available in the public domain. So I spent the last few weeks reading more about this and thought of sharing my understanding

| Metric | Computed | Highlights | Notes |

|---|---|---|---|

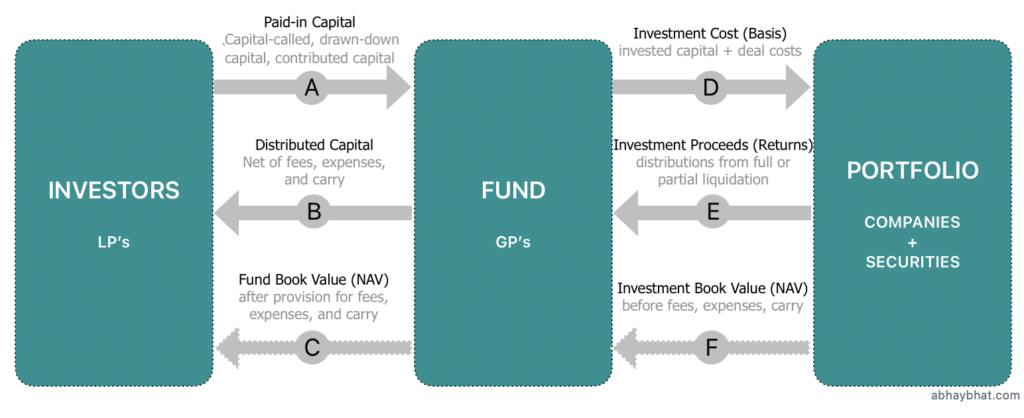

| Multiple on Invested Capital (MOIC) | (E + F) / D | • Best multiple for gauging a GP’s raw investment acumen. • Measures a GP’s ability to invest in big winners (measured as if the GP invested their own dollars). | |

| Gross Total Value to Paid In Capital (Gross TVPI) | (E + F) / A | • Another representation of a GP’s investment acumen. • Measures a GP’s ability to turn LPs’ dollars into big winners (measured as an investment of LPs’ dollars). | |

Net Total Value to Paid In Capital (Net TVPI) | (B + C) /A | • Multiple often quoted by GP’s, but ultimately only the second most important metric for LP’s. | • Less fees, carry and expenses |

Residual Value per Paid In Capital (RVPI) | C / A | • “Paper value” of the fund. • Important metric that can look impressive early in a fund lifecycle. • Ultimately all that matters is how (or whether) RVPI turns into DPI. | • This is where all the shenanigans are done by up-marking the seed-A-B-C…. rounds by frothy valuations |

Distributions per Paid In Capital (DPI) | B / A | • Most important metric to LPs (and by extension GPs) at the end of the fund. | • Realised Value Multiple |

Performance Metrics 101

Distributed to Paid-In Capital (DPI) is a term used to measure the total capital that a private equity fund has returned to its investors. The DPI value is the cumulative value of all investor distributions expressed as a multiple of all the capital paid into the fund up to that time. Distributions are done based on the goal of the fund which typically is 10-12 years. Distributions is actual $ or public market equity shares depending on the appetite and preference of the LP’s.

DPI calculation example

Hypothetical scenario:

- It is 5 years since the fund opened and investors have contributed a total of $50 million.

- The fund has distributed $14.5 million to investors from realised deals.

Calculating the DPI for year 5 would produce the following result:

14.5/50 = 0.29x

This ratio tells us that as of the end of the fifth year, the fund has returned 29 percent of the capital investors have paid so far.

At the end of the fund’s life, all of the year-end DPIs could be shown as follows (in $ millions):

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Distributed Capital ($M) | 0 | 0 | 2 | 12 | 14.5 | 29 | 47.5 | 62.5 | 74.5 | 100 |

| Paid-in Capital ($M) | 30 | 42 | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 50 |

| DPI (at year-end) | 0 | 0 | 0.04x | 0.24x | 0.29x | 0.58x | 0.95x | 1.25x | 1.49x | 2.01x |

Note that often distributed capital is denominate by RVPI until 7/8th year of the fund origination.

Total Value to Paid-In Capital (TVPI)

Total Value to Paid-In Capital (also known as the ‘Investment Multiple’) is a measure of the performance of a private equity fund. It represents the total value of a fund relative to the amount of capital paid into the fund to date.

TVPI thus provides investors with a key metric on the performance of their investment at any point in time. This is particularly useful for a private equity fund since returns consist of both distributed capital and residual holdings, TVPI provides a way to combine both of these and measure them relative to the initial investment.

TVPI Calculation example

TVPI = (Distributed Capital + Residual Value) / (Paid in Capital)

Hypothetical scenario:

- Investors have contributed a total of $50 million to the fund

- The fund has distributed $10 million to investors from realised(exited) deals

- It is 4 years since the fund opened and the residual value of investment assets held by the fund is estimated to be $45.5 million.

Calculating the TVPI for year 4 would:

TVPI Y4 = (10 + 45.5)/50 = 1.11x

10 Year TVPI distribution would like something like this;

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Paid-in Capital ($M) | 30 | 42 | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 50 |

| Distributed Capital ($M) | 0 | 0 | 2 | 10 | 14.5 | 29 | 47.5 | 62.5 | 74.5 | 100.5 |

| Residual Value ($M) | 26 | 30 | 33 | 45.5 | 55.5 | 54 | 46 | 34 | 24.5 | 0 |

| TVPI | 0.87x | 0.71x | 0.70x | 1.11x | 1.40x | 1.66x | 1.87x | 1.94x | 1.98x | 2.01x |

Note that “Residual Value” is notional book value and open to valuation shenanigans which is rampant in early stage venture industry and does not conform to textbook methods like P/E, EBIDTA, EPS , ROIC, EPS, ROCE