Equity Compensation 101

It’s important first to understand the different types of equity compensation, the advantages of each, and how they’re taxed.

Stock options

Stock options allow you to purchase shares in your company’s stocks at a predetermined price, also known as a strike price, for a limited number of years (usually 10). Options come with vesting aka a waiting period before the options, to buy or not, become exercisable. This means that you have to be employed for a certain amount of time — determined by your employer — before you can actually exercise (or buy) the stock you were granted.

The benefit of having stock options is if your business is performing well, the strike price of your stock will be lower than its current market value by the time your options vest. This means you can buy your company stocks for a lower price and sell them at a higher market value. This can become a significant financial gain if the price of your company stocks grows over time. If your business is performing well, then everyone in the business suffers

Restricted stock units

Restricted stock units (RSUs) are the most common type of equity compensation and are typically offered after a private company goes public or reaches a more stable valuation. Like stock options, RSUs vest over time, but unlike stock options, you don’t have to buy them. As soon as they vest, they are no longer restricted and are treated exactly the same as if you had bought your company’s shares in the open market.

In this way, RSUs carry less risk than stock options. As long as your stock price doesn’t drop to $0, they will always be worth something.

In the current times, which can be rightly termed as a ‘normal’ scenario (not referring to high-interest rates, instead its impact on determining investable companies), where businesses can or are expected to go public only if they are being financially more prudent by aiming at one or more of the following

- if they are improving their return on invested capital by burning less cash

- revenue per employee is increasing (typically in software product-driven companies and not infrastructure or heavy industries)

- aiming net profitability by ruthlessly rationing customer acquisition cost and improving long-term value accrual i.e LTC/CAC ratio

The efficiencies summarised are all interlinked and ways of perceiving healthy and sound businesses that are investable in the medium to long term and hence qualified to go public or open to non-accredited retail investors

LTV / CAC Primer

CAC (Customer Acquisition Cost) = The amount spent on each customer acquisition

Accounts for FB ads, Google SEM, AdWords, Instagram, Sales rep, Customer Success rep, Salesforce/Hubspot/Pipedrive licences etc i.e every spend that that is made to acquire customer

LTV (Long-term Value) = (Revenue per customer – CAC) / Churn rate

The ratio LTV / CAC tells us wheather the customer base is profitable or not.

How private stocks are traded ?

The basic tenet of a trade lies in having a seller and buyer and an environment or system where both buyers and sellers can demonstrate their willing to buy or sell stocks without the need to know each other well. This is perfectly established by having a electronic exchange like NASDAQ, NYSE, LSE or NSE. Until a company offers shares to the public, though, the company’s shares are considered private. This means, amongst other things: 1) there is limited liquidity for the shares 2) there are various restrictions on the shares, including SEC requirements for who can buy the shares, how many shareholders the company can have, how long private shareholders have to hold the shares before they can sell, etc.

Once the shares are acquired by investors in various rounds,there are typically 3 categories of share owners for a private business viz; founders, investors and employees. As long as there is no buyer of the stocks money is actually on paper for all the 3 categories of share holders.

Enter “secondaries”

A “secondary” sale is when a shareholder (typically one of the founders or an early employee or an early investor) of a private company sells his or her shares to another buyer. Note this happens w/o an exchange and behind closed doors unlike a public company. This happens within a privileged group of VC, Private equity and accredited investors where the size of the investment is typically $500K – hundreds of millions $.

There is no dilution that happens in secondaries unlike in investment rounds. They are distinguished from a “primary” sale, in which company issues new shares to investors, and the proceeds of that sale go directly into the company.

One of the main reasons why secondaries have become popular is that IPOs have been less common since the crash of 2008. This can be explained by Airbnb, Stripe and bunch of other companies that have decided to stay private for 8+ years for various reasons. Since startups are staying private longer, this means that early founders and employees can’t get liquidity for their shares, sometimes even 5 or 10 years after the company started, even if the company is doing well.

Factors that drive secondaries are:

- supply and demand of the company’s stock. When a company is doing well, investors want to get stock in the company, but a startup may not need the financing or not want to dilute its existing shareholders by selling stock, so its stock may be hard to come by.

- liquidity for early shareholders. Rarely do employees (or even founders) stay at one company for more than a few years, but it’s possible that a succesfull startup may not have an IPO for 5–10 years. It’s not fun to be a millionaire “just on paper”

So who are secondary buyers?

Existing and New Investors.

Some investors even have specific percentage thresholds they are trying to reach (or maintain) — for example, some like to keep a 20% ownership of their companies.

Websites and Micro Funds

These websites require you to be accredited investors Forge, EquityZen, AngelList. SEC Regulation D and JOBS Act are great resources to get started if this interests some one.

Secondary-specific funds

Specific late stage funds focussing on secondaries, as they happen when the startup has achieved significant revenue or traction and is seen as a “leader” in their market space, on the way to an IPO or a major sale. They wouldn’t make as much money as the early investors in those companies, but they would take considerably less risk.

Private Investors, Investment banks and SPV

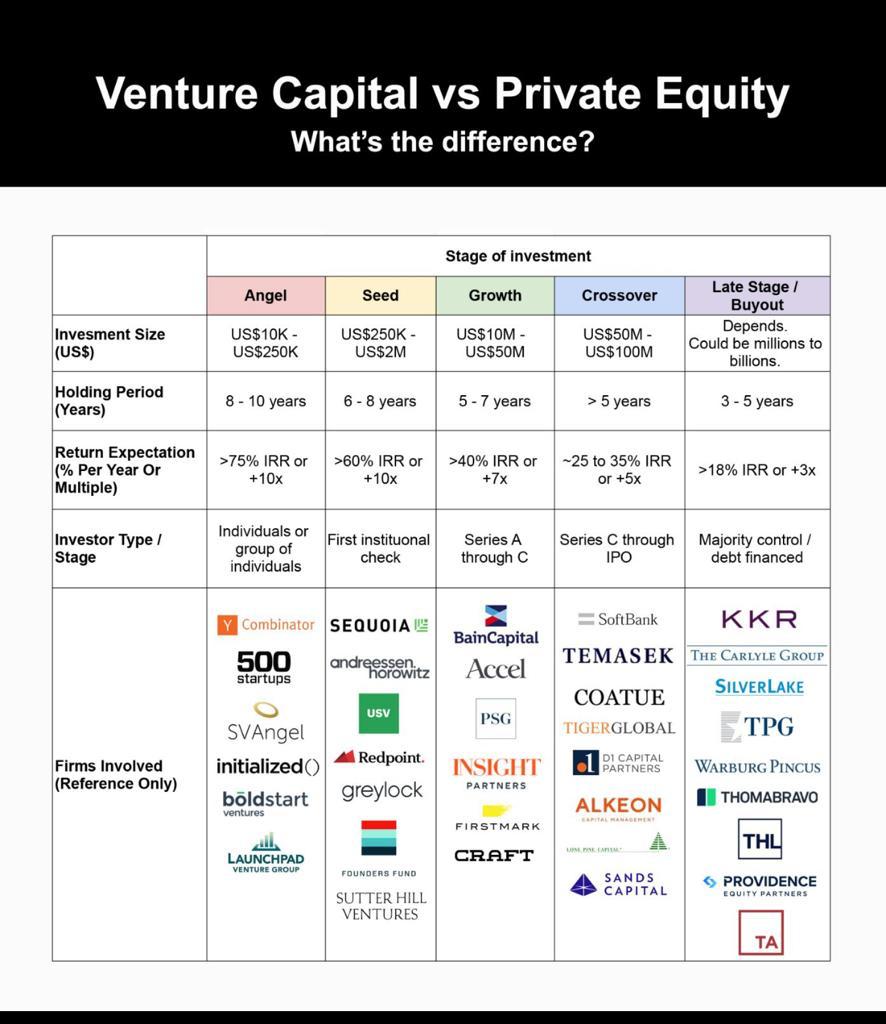

Each stage of investing aims at deploying capital with predetrmined risk-return investment philisophy and commitment they have with their Limited Partners (LP’s)

These were the 2 podcasts, that I highly recommend!

Hope with this write up you were able to get some insights into the early stage operational nuances that play out as the business grows.